Market sentiment has improved on a broad basis, and rather than hunt for recession risks, commentators are praising incoming data as evidence of a broad economic recovery. With cyclicals continuing to gain traction, what does this economic upswing mean for investors? Our research team takes a closer look.

Key take-aways

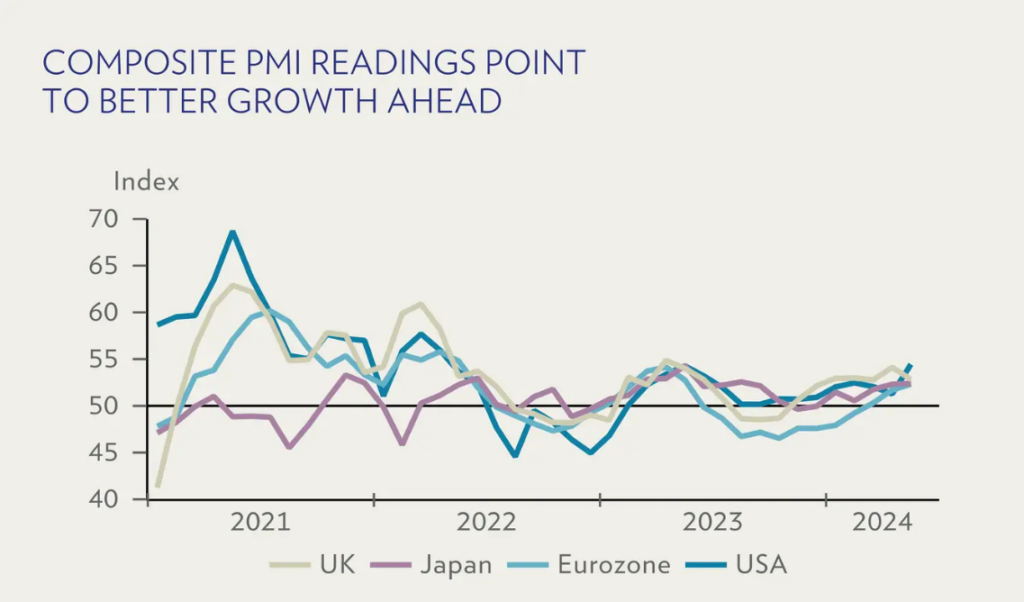

- The PMIs published last week show a perfect amount of increased production to meet demand without the need for more monetary restrictions.

- Further weakening of the Swiss franc appears limited, as rate cuts by large central banks will reduce the franc’s rate disadvantage.

- The artificial intelligence investment cycle is still in the early innings, and the path to monetisation of products will be key.

The economic upswing is gaining momentum – at least, that is the message from the purchasing managers’ indices (PMIs) survey published last week. The available data shows a perfect amount of increased production to meet demand without causing bottlenecks that would warrant more monetary restrictions. Furthermore, we reject the notion that the higher PMIs herald interest rate hikes; we do not expect any in the US nor in the eurozone, where the chances for a June rate cut are still intact.

Since the beginning of the year, the CHF has weakened by roughly 6% vs the EUR and by 8% vs the USD, making it the weakest G10 currency this year after the JPY. However, room for further weakening appears limited, as rate cuts by the large central banks will reduce the franc’s rate disadvantage. In the longer term, the franc’s uptrend due to relative price stability and its safe haven characteristics are likely to remain intact.

Continuing with the upswing narrative, in the artificial intelligence (AI) space there is no end to the AI investment boom on our radar. However, it will take time for the productivity gains to filter through to the broader economy.

PMIs point to improved economic outlook

Preliminary results from the May PMI surveys point to accelerating demand and ample supply, suggesting stronger growth with moderate inflation. Industrial activity in the US continues to expand at a moderate pace, while Europe is showing clear signs of bottoming out. Price pressures remain moderate overall, with industrial prices falling in Europe and services prices rising at a slower pace.

The PMI surveys point to an improved economic outlook. The preliminary May results show some acceleration in economic growth. Industrial activity in Europe is improving and starting to close the gap with the US survey results, which is encouraging. US industrial activity remains just above the 50 level that marks the boundary between expansion and contraction. Thus, the survey results point to a moderate cyclical expansion in the US and a clear bottoming out of the industrial slowdown in the eurozone, with the UK and Japan moving from contraction to expansion in industrial activity, making the global growth outlook more balanced.

The details of the PMI surveys are also positive. Price pressures remain moderate in a number of places, with industrial output prices in the eurozone in contractionary mode and price pressures in services easing. Input prices in services tend to lead inflation, and the latest figures support our view that inflation will move closer to 2% in the coming months in both the US and the eurozone. Moreover, the latest PMI readings suggest that demand is accelerating overall, while supply-related details show ample supply, pointing to better growth with moderate inflation.

Cloud computing and AI: No signs of fatigue

The latest Q1 earnings results from the leading semiconductor companies confirm that the AI investment cycle is in full swing, with no signs of fatigue. On the contrary, the momentum has increased. We are still in the early innings of a long-term investment story. In this phase, we are seeing massive investments in the AI infrastructure, as data centres need to be upgraded to host AI workloads. Therefore, the largest beneficiaries are semiconductor companies with high demand for leading-edge chips, such as AI accelerators, high-bandwidth memory, and networking equipment.

While cloud service providers are increasing their investments, they are also benefiting from an acceleration in cloud revenues, which is a positive signal for the sustainability of the cycle. Furthermore, the number of software vendors that have announced AI-powered products and applications is encouraging, and this should allow for further penetration of AI into our lives and economy. That said, the monetisation of AI products is still a long way away, and it is the only area that lacks visibility and where we need to build more confidence going forward. While we are generally encouraged by the monetisation strategy of some early AI adopters, we want this to be reflected in surging revenues for software companies. So far, information technology spending has been weak, as companies have rationalised their cost base following the Covid-19 over-hangs, but we expect to see improvements going forward.

What does this mean for investors?

Market sentiment has improved on a broad basis. We are far away from having to worry about interest rate hikes, and we maintain our call for a June interest rate cut in the eurozone. Our view on AI as a key investment theme also remains unchanged.

The latest earnings results have confirmed our view that the AI investment cycle is still in the early innings, with no signs of fatigue. That said, the path to monetisation of artificial intelligence products will be key. We maintain our positive view on Cloud Computing & Artificial Intelligence from a thematic perspective and on information technology and communication services form a sectoral perspective.